Annual Report & Accounts 2026

60

Whilst these do not meet the definition under IAS 1 of significant accounting estimates or critical accounting judgement, the recognition of certain material assets and liabilities is based on assumptions and/or is subject to longer-term uncertainties. The other areas of judgement and accounting estimates are set out below.

RECOVERABILITY OF TRADE RECEIVABLES (note 17)

Due to the nature of the business, there are high levels of trade receivables at the year end and, therefore, a risk that some of these balances may be irrecoverable. Because amounts due to lawyers are only payable when the Group has been paid, there is a built-in hedge to this exposure to the extent of approximately 75%. A variance of 1% in the loss ratio reflected in the impairment provision would equate to a movement in trade receivables impairment of £211,021 (2026: £172,840) which, in turn, would result in a change in the corresponding reduction in trade payables of £158,265 (2026: £129,630) and an impact to profit of £52,755 (2026: £43,210).

WORK IN PROGRESS (ACCRUED INCOME) (note 17) AND ASSOCIATED ACCRUED LIABILITY (Note 21)

During each financial year, the business carries out a review of billing activity to identify what share of each month’s billing relates to a period prior to the start of that financial year. The results of these reviews are then added to the data derived from similar reviews in previous financial years and demonstrate a materially consistent performance insofar as to the share of each given month’s billing which relates to a prior financial year. A fundamental judgement made when performing these reviews is that the contracts entered into each year have performance obligations with similar characteristics to those entered into in previous years; for example that the value of the services provided to the client is transferred evenly over the period of time that the services are provided. We use this data to generate a profile of the share of post year-end billing which relates to a previous financial year. This profile is then applied to the current year’s budgeted billing to calculate the gross value of accrued income at the year end, a further adjustment is made to this value to reflect the expected credit loss, this adjustment is not material and as such is not separately disclosed. The accrued income valuation is then validated by reviewing the actual billing between the year end and the time the accounts are prepared (representing approximately 60% of the value of accrued income) to ensure that actual performance is in line with the expected profile. Keystone’s lawyers’ fees are 100% variable and directly associated with the value of fee income produced. Accordingly, when the Group recognises a value of accrued income, it also recognises a directly associated accrued liability in respect of the fees payable to its lawyers for that work which equates to approximately 75% of the value of accrued income. Were the actual billing to differ to the budget but all other things remained equal, then a 1% variance in billing would equate to a movement in revenue of £146,088 (2026: £79,464). This, in turn, would result in a change in the associated cost of sale of £109,566 (2026: £59,362) and an impact to profit of £36,996 (2026: £20,102).

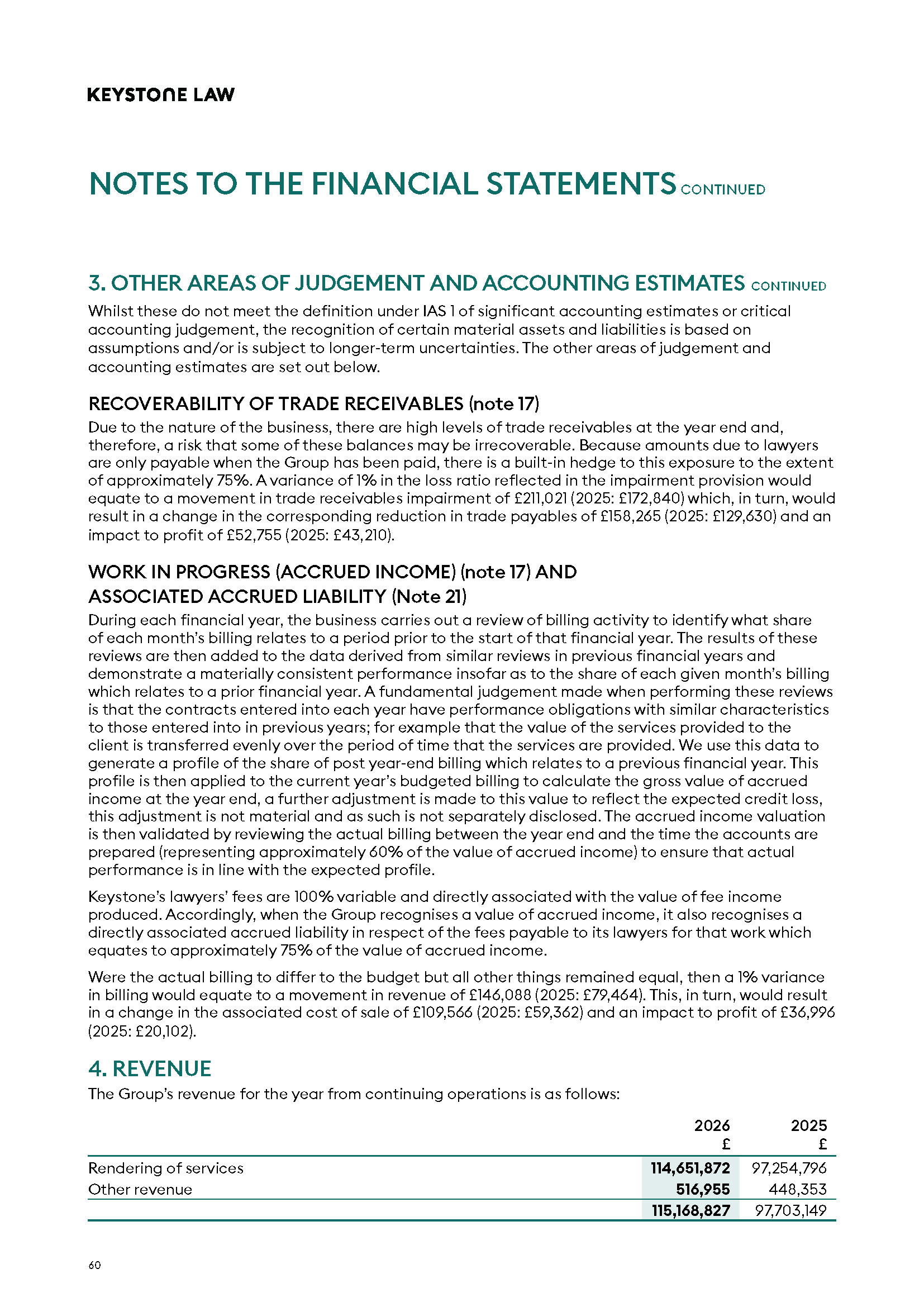

4. REVENUE

The Group’s revenue for the year from continuing operations is as follows:

2026 £

2026 £

Rendering of services

114,651,872

97,254,796

Other revenue

516,955

448,353

115,168,827

97,703,149

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

3. OTHER AREAS OF JUDGEMENT AND ACCOUNTING ESTIMATES CONTINUED

Whilst these do not meet the definition under IAS 1 of significant accounting estimates or critical accounting judgement, the recognition of certain material assets and liabilities is based on assumptions and/or is subject to longer-term uncertainties. The other areas of judgement and accounting estimates are set out below.

RECOVERABILITY OF TRADE RECEIVABLES (note 17)

Due to the nature of the business, there are high levels of trade receivables at the year end and, therefore, a risk that some of these balances may be irrecoverable. Because amounts due to lawyers are only payable when the Group has been paid, there is a built-in hedge to this exposure to the extent of approximately 75%. A variance of 1% in the loss ratio reflected in the impairment provision would equate to a movement in trade receivables impairment of £211,021 (2026: £172,840) which, in turn, would result in a change in the corresponding reduction in trade payables of £158,265 (2026: £129,630) and an impact to profit of £52,755 (2026: £43,210).

WORK IN PROGRESS (ACCRUED INCOME) (note 17) AND ASSOCIATED ACCRUED LIABILITY (Note 21)

During each financial year, the business carries out a review of billing activity to identify what share of each month’s billing relates to a period prior to the start of that financial year. The results of these reviews are then added to the data derived from similar reviews in previous financial years and demonstrate a materially consistent performance insofar as to the share of each given month’s billing which relates to a prior financial year. A fundamental judgement made when performing these reviews is that the contracts entered into each year have performance obligations with similar characteristics to those entered into in previous years; for example that the value of the services provided to the client is transferred evenly over the period of time that the services are provided. We use this data to generate a profile of the share of post year-end billing which relates to a previous financial year. This profile is then applied to the current year’s budgeted billing to calculate the gross value of accrued income at the year end, a further adjustment is made to this value to reflect the expected credit loss, this adjustment is not material and as such is not separately disclosed. The accrued income valuation is then validated by reviewing the actual billing between the year end and the time the accounts are prepared (representing approximately 60% of the value of accrued income) to ensure that actual performance is in line with the expected profile. Keystone’s lawyers’ fees are 100% variable and directly associated with the value of fee income produced. Accordingly, when the Group recognises a value of accrued income, it also recognises a directly associated accrued liability in respect of the fees payable to its lawyers for that work which equates to approximately 75% of the value of accrued income. Were the actual billing to differ to the budget but all other things remained equal, then a 1% variance in billing would equate to a movement in revenue of £146,088 (2026: £79,464). This, in turn, would result in a change in the associated cost of sale of £109,566 (2026: £59,362) and an impact to profit of £36,996 (2026: £20,102).

4. REVENUE

The Group’s revenue for the year from continuing operations is as follows:

2026 £

2026 £

Rendering of services

114,651,872

97,254,796

Other revenue

516,955

448,353

115,168,827

97,703,149

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

3. OTHER AREAS OF JUDGEMENT AND ACCOUNTING ESTIMATES CONTINUED