Annual Report & Accounts 2026

43

OUR GOVERNANCE

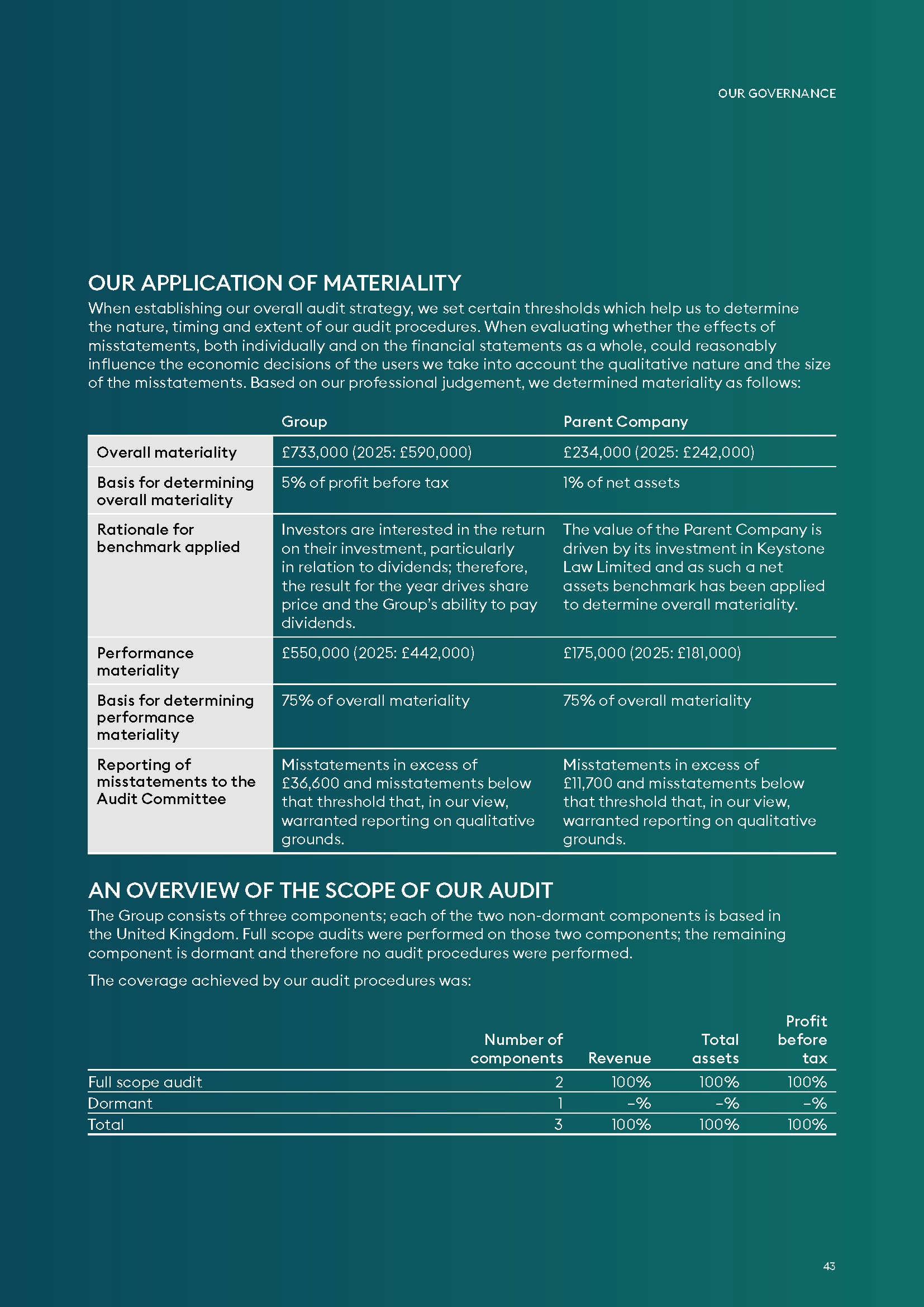

OUR APPLICATION OF MATERIALITY

When establishing our overall audit strategy, we set certain thresholds which help us to determine the nature, timing and extent of our audit procedures. When evaluating whether the effects of misstatements, both individually and on the financial statements as a whole, could reasonably influence the economic decisions of the users we take into account the qualitative nature and the size of the misstatements. Based on our professional judgement, we determined materiality as follows:

Group

Parent Company

Overall materiality

£733,000 (2026: £590,000)

£234,000 (2026: £242,000)

Basis for determining overall materiality

5% of profit before tax

1% of net assets

Rationale for benchmark applied

Investors are interested in the return on their investment, particularly in relation to dividends; therefore, the result for the year drives share price and the Group’s ability to pay dividends.

The value of the Parent Company is driven by its investment in Keystone Law Limited and as such a net assets benchmark has been applied to determine overall materiality.

Performance materiality

£550,000 (2026: £442,000)

£175,000 (2026: £181,000)

Basis for determining performance materiality

75% of overall materiality

75% of overall materiality

Reporting of misstatements to the Audit Committee

Misstatements in excess of £36,600 and misstatements below that threshold that, in our view, warranted reporting on qualitative grounds. Misstatements in excess of £11,700 and misstatements below that threshold that, in our view, warranted reporting on qualitative grounds. AN OVERVIEW OF THE SCOPE OF OUR AUDIT The Group consists of three components; each of the two non-dormant components is based in the United Kingdom. Full scope audits were performed on those two components; the remaining component is dormant and therefore no audit procedures were performed. The coverage achieved by our audit procedures was:

Number of components

Revenue

Total assets

Profit before tax

Full scope audit

2

100%

100%

100%

Dormant 1

–%

–%

–%

Total

3

100%

100%

100%

OUR GOVERNANCE

OUR APPLICATION OF MATERIALITY

When establishing our overall audit strategy, we set certain thresholds which help us to determine the nature, timing and extent of our audit procedures. When evaluating whether the effects of misstatements, both individually and on the financial statements as a whole, could reasonably influence the economic decisions of the users we take into account the qualitative nature and the size of the misstatements. Based on our professional judgement, we determined materiality as follows:

Group

Parent Company

Overall materiality

£733,000 (2026: £590,000)

£234,000 (2026: £242,000)

Basis for determining overall materiality

5% of profit before tax

1% of net assets

Rationale for benchmark applied

Investors are interested in the return on their investment, particularly in relation to dividends; therefore, the result for the year drives share price and the Group’s ability to pay dividends.

The value of the Parent Company is driven by its investment in Keystone Law Limited and as such a net assets benchmark has been applied to determine overall materiality.

Performance materiality

£550,000 (2026: £442,000)

£175,000 (2026: £181,000)

Basis for determining performance materiality

75% of overall materiality

75% of overall materiality

Reporting of misstatements to the Audit Committee

Misstatements in excess of £36,600 and misstatements below that threshold that, in our view, warranted reporting on qualitative grounds. Misstatements in excess of £11,700 and misstatements below that threshold that, in our view, warranted reporting on qualitative grounds. AN OVERVIEW OF THE SCOPE OF OUR AUDIT The Group consists of three components; each of the two non-dormant components is based in the United Kingdom. Full scope audits were performed on those two components; the remaining component is dormant and therefore no audit procedures were performed. The coverage achieved by our audit procedures was:

Number of components

Revenue

Total assets

Profit before tax

Full scope audit

2

100%

100%

100%

Dormant 1

–%

–%

–%

Total

3

100%

100%

100%